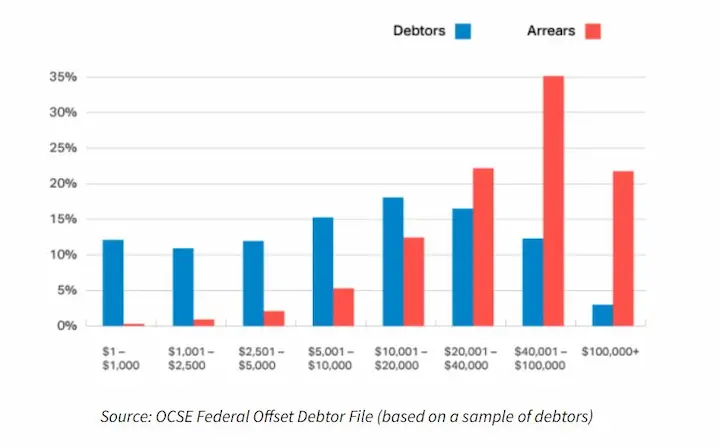

Child support payments are a significant financial burden for many parents. The court mandates such payments to verify that children receive adequate care and support, but it is not uncommon for paying parents to struggle with meeting their obligations.

Payday loans are short-term borrowing options with high-interest rates and fees. Lenders market them as quick solutions to urgent cash needs, but they trap borrowers in cycles of debt due to their predatory practices. Many people explore payday loans to supplement their income and make timely child support payments in such situations, especially when they have poor credit.

Most parents feel they have no choice but to turn to payday loans when they fall behind on child support payments. PaydayDaze explores if it is a viable option and what alternatives exist for people struggling with child support payments.

Understanding Payday Loans

The desire to provide for one’s children is a powerful motivator. Sometimes the financial burden of child support payments is overwhelming. Most individuals explore using payday loans to meet their obligations in such situations. But before doing so, understand such loans’ eligibility criteria and legal implications. Payday loan eligibility requirements vary by state and lender but generally include the following.

- Being at least 18 years old.

- Having a valid ID.

- Proof of employment.

- An active bank account.

Just because you meet the criteria does not necessarily mean you must obtain a payday loan. As part of the loan agreement, you must weigh the risks against the benefits while exploring potential long-term consequences on credit scores or future loan opportunities. Loan terms and the type of loan can make a big difference in deciding the best course of action. Various states have strict regulations regarding payday lending practices that borrowers must know before entering such agreements.

Legal implications exist to address before obtaining any extra debts if child support payments are in arrears. Seeking financial literacy education or credit counseling services can offer alternative solutions, like devising a proper repayment plan, and help prevent further financial struggles.

Careful review is necessary on all available options instead of immediately turning to payday loans to solve child support payment woes. Understanding payday loan eligibility requirements and legal considerations is key before borrowing money through such a channel.

Improving financial literacy skills and seeking guidance from knowledgeable professionals positively impacts short- and long-term goals for managing finances effectively while supporting children’s needs without creating unnecessary debt burdens. American borrowers spend close to $7.4 billion on payday loans annually, according to MoneyTransfers.com. The table below contains more payday loan statistics.

| Fact | Value |

|---|---|

| Annual spending on payday loans in the US | $7.4 billion |

| Median income reported in US payday loan applications | $22,476 |

| Percentage of American borrowers with 11-19 payday loans per year | 34% |

| Percentage of Americans citing recurring expenses as the reason for a first payday loan | 69% |

| Average APR of a $300 payday loan in Texas | 664% |

| Percentage of Americans aged 25-29 who have taken out a payday loan | 9% |

| Percentage of American households with $15,000-$25,000 income that is payday loan borrowers | 11% |

The High Cost Of Payday Loans

Understanding payday loans is key before deciding on borrowing a loan. Obtaining a payday loan to help with child support payments seems easy, but it leads to financial strain and a further debt cycle.

Payday loans are known for their high-interest rates and hidden fees, which make it challenging for borrowers to repay the loan. Predatory lending practices by payday lenders are usually under scrutiny due to their negative impact on consumers’ finances.

Such lenders’ exorbitant interest rates and hidden fees usually trap low-income individuals in a vicious debt cycle, especially when dealing with late payments. Most Borrowers of payday loans renew their loans because of a financial emergency and constraints, leading them into more significant financial trouble than when they first took out the loan.

Short-Term Repayment Requirements

Borrower Eligibility Criteria for obtaining a payday loan require proof of sources of income, a valid checking account, and a valid ID. Loan Repayment Periods for payday loans are generally due on the next payday or within two to four weeks, making it crucial for borrowers to manage their monthly payments.

Payday loan lenders require borrowers to write a post-dated check for the loan amount or allow automatic withdrawal from the borrower’s account. Payday lenders charge a fee for loan origination, and the interest rate is usually higher than traditional loans. Many of them offer online application processes for added convenience.

Borrower Eligibility Criteria

The first factor that lenders look at is income requirements. Borrowers must provide proof of steady income or employment status to be eligible for a short-term loan. It helps to verify that the borrower repays the loan on time without defaulting.

Lenders review the borrowers’ credit history and outstanding debts, along with meeting income requirements. Lenders usually review an individual’s credit score before approving an online application for a loan. Factors such as late payments or high levels of debt impact their eligibility for a payday loan If there are any red flags on their record.

Legal obligations such as child support payments are necessary to determine if someone is eligible for a short-term loan. Potential borrowers must carefully evaluate such factors before deciding if a payday loan suits them in a financial emergency.

Loan Repayment Periods

Moving on to the topic of short-term repayment requirements, another key factor that borrowers must review is the loan repayment period. Various lenders offer flexible repayment options such as longer payment plans or grace periods. Payday loans have a shorter repayment period than other types of loans, usually from two weeks to a few months, which might affect the borrower’s ability to manage their monthly payments adequately.

Borrowers must carefully review and understand their lender’s specific terms regarding loan payments. Interest rates on payday loans are high, and late fees apply if you delay payments. Creating a budget and planning for loan payments helps prevent borrowers from further financial trouble with basic household expenses.

Understanding the loan repayment period and taking advantage of any available flexibility in payment plans enables individuals to make a well-informed loan decision if a payday loan is right for them.

Alternatives To Payday Loans

There are various alternatives to payday loans.

- Budgeting is an effective alternative to payday loans, as it allows individuals to plan their finances, identify areas where they must cut expenses, and prioritize their spending. This can help borrowers avoid needing a loan request with high-interest rates on payday loans.

- Savings are an effective alternative, as it provides an accessible source of funds if individuals set aside money regularly, reducing the need for access to payday loans.

- Credit Unions offer a payday loan alternative: short-term, low-interest loans with more flexible repayment terms than payday lenders. They are a viable option for people looking for an alternative solution to access payday loans. Credit Unions provide financial education and other services that help individuals manage their financial resources more effectively. They offer an alternative to payday loans that provide greater financial security in the long run.

Budgeting

Managing child support payments is a challenging task for many parents. Obtaining payday loans is not the best solution to address such a financial burden. Budgeting and financial planning are essential tools that help you manage your income and expenses more effectively, including basic household expenses.

Creating a budget is key to managing child support payments. It involves tracking your income and expenses to determine how much money you have left after covering your essential needs, such as housing, food, transportation, and utilities. Doing so helps you identify areas where you need to spend more on non-essential items to save money and avoid the need for loan requests with high-interest rates.

Saving strategies such as setting aside monthly money towards an emergency fund or retirement account help you avoid relying on expensive payday loans when unexpected costs arise, such as additional expenses or medical expenses. Strong budgeting and expense-tracking skills combined with sound financial management principles like saving strategies enable you to take control of your finances without costly loan options like small, short-term loans.

It sometimes seems tempting to turn to payday loans while mounting child support payment obligations, but there are viable alternatives worth reviewing instead. Financial planning and effective income management techniques like budgeting offer practical solutions that alleviate the stress associated with debt and provide long-term benefits such as greater financial stability over time. This can be particularly helpful in navigating a child support arrangement.

Savings

Budgeting strategies help manage child support payments and reduce expenses. Creating an emergency fund is key to avoiding payday loans. You must have at least three to six months’ worth of living expenses saved up for emergencies. Automatic savings towards such an account each month provide a financial cushion when unexpected costs arise, such as medical expenses or car repairs.

Retirement planning is another way to avoid relying on high-interest loans. Setting aside money regularly into a retirement account enables you to prepare for the future and reduce the temptation to use credit cards or borrow from lenders, such as those offering small, short-term loans.

Credit Unions

Another alternative to payday loans is using credit unions. Credit unions are non-profit financial institutions that offer services similar to traditional banks but with lower fees and better interest rates for members. Membership eligibility varies by credit union but generally requires living or working in a certain geographic area, being employed by a specific organization, or having a family member who is already a member. These options often serve as better financial solutions than small, short-term loans or high-interest rates and fees in times of need.

The main benefit of credit unions is their loan options. They provide small-dollar loans with reasonable terms and interest rates compared to predatory lenders like payday loan companies. Credit unions prioritize customer service experience because they belong to their members rather than shareholders seeking profit. It means that decisions made at the credit union level must benefit its membership base rather than maximize profits for investors. With the rise of online lenders and applications for loans, credit unions may also provide better chances of loan approval than other options.

Assessing Your Financial Situation

Most people use payday loans to solve their financial woes. However, obtaining a payday loan is not usually the best idea, leading to even more problems. Consider if an option for payday loan is necessary while being aware of the applicable payday loan laws. The following is a simple process to help you evaluate your financial situation.

- Take time to assess your financial situation before attempting to access payday loans or obtaining a loan.

- Evaluate your budgeting strategies and see if there are any areas where you must cut back on expenses. Explore all income sources, such as part-time jobs or consulting gigs, that help supplement your regular earnings.

- Look into debt management options and legal alternatives before borrowing money from lenders who charge high-interest rates, especially when considering applications for loans with various online lenders.

Making An Informed Decision

Reviewing legal implications is necessary before obtaining a payday loan for child support payments. Various states have applicable payday loan laws prohibiting using loans to pay off child support obligations, while others allow it under certain circumstances. You must check with local regulations and seek legal advice before making decisions.

Available resources such as government assistance programs or negotiations with the custodial parent are necessary before resorting to an option for a payday loan. Evaluating loan eligibility and repayment options are key steps in ensuring that the borrower can afford the loan without becoming trapped in a cycle of debt, and it also helps in improving your chances of loan approval.

Conclusion

Seeking alternatives to payday loans and making informed decisions are crucial in managing financial stability. Carefully assessing your financial situation, considering the applicable payday loan laws, and exploring debt management solutions can help you avoid the pitfalls of payday loans. Additionally, remember to evaluate the variety of applications for loans available and choose the best online lenders for your needs to ensure better loan terms and interest rates.

It is tempting to review an internet-based payday loan as a means of making child support payments, but the high costs and short-term repayment requirements must give pause. You must assess your financial situation honestly before making such a key decision. With annual percentage rates often being very high and the need to repay the loan proceeds quickly, these loans can lead to long-term financial consequences.

Alternative options include seeking assistance from family or friends or exploring community resources for financial aid. While obtaining a payday loan from a network of lenders provides temporary relief, it’s essential to consider your payment history and the potential for needing additional payday loans in the future. Making an informed decision about how best to manage child support payments requires careful review and planning.

Frequently Asked Questions

How many recent pay stubs are typically required when applying for a payday loan?

Most payday lenders require 1-2 recent pay stubs when applying for a loan. The pay stubs provide proof of income and employment. Some lenders may accept only one current pay stub while others ask for two consecutive stubs spanning within the last 30-60 days to demonstrate a regular income stream.

Is there a specific number of pay stubs I need to provide to qualify for a payday loan?

There is no universal number of pay stubs required, as it varies by lender. Typically, you need to provide either one current pay stub or your most recent 1-2 consecutive pay stubs to qualify. Having at least one complete, current pay stub demonstrates employment and income level for loan approval. More pay stubs may help verify regular income.

Can I use electronic pay stubs or digital copies, or do I need physical copies for my payday loan application?

Most payday lenders accept digital and electronic versions of pay stubs from applicants. Taking photos of physical pay stubs or using PDFs of digital stubs are standard options. Screenshots of online pay stubs also often qualify. As long as the copies clearly show all needed employment and income details, they can substitute for physical stubs.

Do payday loan lenders have different requirements for the number of pay stubs, or is it a standard practice across all lenders?

Payday loan lender requirements for number of pay stubs can vary. Some ask for only the most current stub, while others require two consecutive stubs from the last 30-60 days. Policies differ by lender and there is no completely standardized practice. Applicants should verify specific stub requirements before applying for the loan.

What should I do if I don’t have enough recent pay stubs for a payday loan application?

If you lack enough recent pay stubs for a payday loan, options include providing bank statements showing direct deposit history to prove income, asking your employer to print new pay stubs, providing a written employment verification letter, or delaying your application until you have the required pay stubs.