Auto title loans or a loan on car title seem to be the fast and simple solution if you find yourself in a cash-dry situation. In this process, you commit the title of your fully paid-off vehicle, and in return, you obtain instant cash. Lenders provide short-term loans quickly and easily. Sounds quite a deal, right?

Tread carefully. Title loans, including online title loans, pose significant ramifications and expenses that are more harmful than good if you don’t take sufficient precautions. Title loan companies market the loans as speedy cash for unforeseen circumstances; they best serve as a last resort.

The thorough guide illuminates every detail of the so-called car title loans, encapsulating:

- What exactly the loans are, and how do they function?

- What are the demographics that opt for the loans and their reasons?

- The advantages and disadvantages of procuring a title loan.

- Hidden risks and charges to be vigilant about.

- Alternatives to costly title lending.

- Shrewd strategies to shield yourself upon taking a title loan.

- Frequently inquired queries.

Now, let’s decipher the essentials.

What Is an Auto Title Loan Exactly? Online Title Loans Explained?

A title loan—a.k.a. a motor vehicle title loan—is a specific secured loan. In this, you are able to use your fully paid-off car, truck, motorcycle, RV, or any other vehicle as a pledge to borrow funds. The lender institutes a lien on your car title in reciprocation for offering you a loan amount in cash.

The process pans out like this:

- You coordinate a meeting with a title loan provider—a bank, online title loan service, or title loan companies—and present your vehicle’s title (referred to as a pink slip), which must exhibit 100% ownership on your part. Your vehicle’s title must be void of any existing liens or loans.

- The lender proceeds with a swift inspection of your vehicle and asks you for a key copy. They aim to confirm your vehicle is in satisfactory condition and possess it.

- Once approved, you ratify loan documents authorizing the lender to institute a lien on the title, which endows them with the legal right to reclaim and sell their vehicle if you default on the loan.

- The lender furnishes you with a loan amount approximately equal to 25-50% of your vehicle’s resale value. In the case of car title loans, the older your vehicle, the lower the loan amount.

- To avail of this type of loan, you’ll need to hand over a spare set of car keys and the pink slip until you repay the instant online title loan.

- Title loan lenders provide loans usually with terms of 30 days or less. The full emergency title loan amount and interest and fees are required as a lump sum when the term is up.

A title loan allows you to temporarily trade the equity in your vehicle for quick cash. But failing to repay it means losing your car.

Who Seeks Car Title Loans Near Me and Why? Loan on Car Title Demographics?

Certain types of borrowers tend to be attracted to title loans near me versus other sources of financing. Here are the main reasons people seek out risky, high-cost loans:

1. Poor credit history – Title lenders don’t run credit checks or look at FICO scores, which makes car title loans no credit check one of the few borrowing options open to people with very low credit scores who do not qualify with most banks or lenders.

2. Need fast cash – The instant online title loan process is quick, with money handed over almost immediately after approval. There’s no waiting for bank approvals. Instant loan funding helps people who need money immediately to cover an emergency expense or overdue bills before their next paycheck.

3. Own a vehicle free and clear – To procure a title loan, you must legally own your car with no existing liens to use as collateral. People still making payments on their vehicles do not qualify.

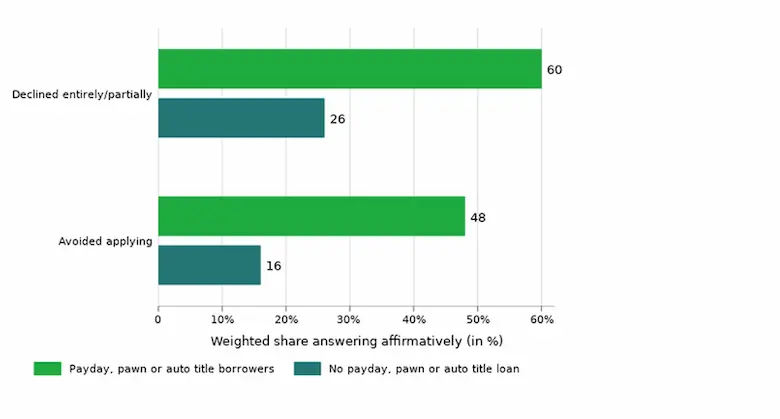

4. Few other options – For people with maxed-out credit cards, high-interest payday loans, and no assets besides their car, a title loan is one of the only remaining ways to access cash in a bind.

5. Sub-prime borrowing – Title loan lenders cater specifically to risky subprime borrowers who do not qualify for better rates elsewhere, which allows them to charge excessively high interest rates.

6. Repeated borrowing – Once in title loan debt, many borrowers end up rolling over loans or reborrowing in subsequent months to make ends meet by availing more of the emergency title loans.

Title loans, including car title loans near me, are able to meet the need for immediate funds among high-risk borrowers with poor or bad credit; their potential harm usually outweighs their advantages. Their questionable worth largely stems from their application process and their annual percentage rate, both of which are geared more towards benefiting the lender over the borrower.

The Ebbs and Flows of Auto Title Loans and Car Title Loans Near Me

Title loans offer immediate benefits, but there exist serious drawbacks with long-lasting impacts that warrant thorough understanding.

The Pros

- Speedy financing – Title lenders offer quick access to cash with limited approval requirements and no formal credit checks, providing an attractive option for people looking for same day funds. Some lenders even guarantee you approval.

- Continued utilization of your vehicle – You have the right to continue driving your vehicle while making payments on the loan when you take a title loan. The lender only reclaims your vehicle if you default.

- High approval odds – Compared to their peers, like banks and personal loan providers, title lenders have relatively higher approval rates thanks to the collateral involved.

- No impact on your credit – As title loans don’t necessitate a formal credit check, they have no direct effect on your credit score. Defaulting on your payments impacts your score negatively.

The Cons

- Exorbitant APR – Title loan interest rates normally begin around 100% APR and surpass 300% APR. The high annual percentage rate makes it financially difficult to settle the debt.

- Short loan terms – Title loans have to be paid back within 30 days, which forces borrowers to scramble to amass a hefty lump sum payment in a short duration, leading to the rolling over of loans and the accrual of more interest and fees.

- Threat of repossession – Defaulting on your repayments empowers the lender to confiscate and auction your vehicle, leaving you without a mode of transportation.

- Overpriced fees – Over and above the interest, lenders levy steep origination fees, processing fees, and late fees that raise the true expense associated with the loan. Read the loan terms before committing.

- Predatory lending – Advocates for customers argue that title lenders target low-income, minority populations exploitatively with the loan options.

- Stringent regulations – Only 16 states permit auto title loans, while the rest have banned or regulated them due to their predatory nature. Even in places where they’re legal, the rates remain sky-high.

You get tempted by the allure of title loan places near me if you are seeking a solution for a financial emergency. Short repayment periods that set borrowers on a collision course with default with interest rates deemed excessive for banks and the ever-present risk of losing your vehicle, title loans are categorized among the most high-risk lending options available.

Hidden Dangers and Payment Stings in Online Title Loans and Loan on Car Title to Look Out For

Besides the basic merits and demerits of this financial approach, be conscious of underlying yet significant risks with dealing with a title lender:

- Balloon payments – The prospects of repaying the entire loan as a single payment after only 30 days turn unfeasible for several borrowers. The predicament propels them into continuously renewing loans and spiraling debts.

- Interest-only payments – Lenders offer interest-only payments for the first month or two, adding more interest to the loan before you even start paying off the principal amount.

- Fast title transfers – Defaulters only have a narrow window (roughly 1-2 days) to fully settle the loan before their vehicle title is hastily signed over to the lender.

- Aggressive collections – Certain lenders resort to extreme methods, from incessant calls and persistent letters to turning up at your residence or place of work solely to collect on defaulted loans.

- Junk fees – Watch out for hidden fees like processing charges, document fees, and rollback fees, which tend to be buried in your loan agreement. Please read carefully.

- Deceptive advertising – Remain cautious of promotions that glorify “no credit check” without outlining the adverse attributes of title lending compared to other alternatives.

- Reborrowing – It’s almost normal for borrowers to secure a new title loan immediately after settling the old one, recommencing the costly cycle.

- Incorrect valuations – Other lenders dispense less than the actual loan amounts, underestimating your vehicle’s resale value. Do your due diligence with Kelley Blue Book valuations in advance.

- Add-on products – Lenders pressure you to incorporate add-ons, such as roadside assistance, which inflate the loan amount but offer meager value.

It’s necessary to weigh the risks of complex payment structures and potentially hidden fees if you’re looking for the best title loans. Keep the idea of competitive title loans in the back of your mind, as the drawbacks tend to make the loans less competitive than they appear at first glance.

Title lenders tend to have fewer restrictions and regulations, increasing the risk implications for your business. It’s necessary to have a careful examination of your options, read reviews, compare loan terms, and thoroughly research lenders.

Alternatives to High-Cost Auto Title Loans and Title Loan Places Near Me

Given the risky nature of title loans for fast access to emergency cash, it’s necessary to understand this as a very last resort. Here are alternative options to manage an unexpected expense before resorting to precarious, unsecured loans:

Borrow from family or friends – They offer to lend you money if you have trusted people in your life. Personal loans agreed-upon terms are a much more affordable and flexible solution than dealing with a title loan verification agent.

Credit cards – Even though credit card cash advances have high rates and fees, they’re still less onerous than title loans. The option to repay in installments over time eases financial pressure.

Traditional loans – Various financial institutions like banks, credit unions, and online lenders offer installment loans and personal lines of credit with more reasonable rates than title lending. Fair credit is generally required to qualify.

Home equity loans – Homeowners with available equity have the option of a cash-out refinance, HELOC, or home equity loan. These provide funds at low rates compared to unsecured loans like title loans.

Payment plans – Many service providers cooperate to establish a payment plan for costs like medical bills, which are far less daunting than a single substantial sum.

Credit counseling – Numerous nonprofit credit counseling services offer free education, help with budgeting, and advice on how to manage various debts and expenses through strategies like debt consolidation.

Government assistance – There are many Federal, state, and local programs to aid with essentials like food, rent, utilities, and healthcare. Check out what assistance is available in your locality.

Smaller payday loans – Payday loans for smaller amounts tend to pose a lesser risk than title loans. Use sparingly and only if no other options remain.

401k/retirement loan – Borrowing against your retirement savings is not ideal; it is less harmful than risking your vehicle, especially if your situation leaves you with no other alternative to get quick cash. A simple online request form is usually the process at financial institutions.

Peer-to-peer loans – Web platforms such as Prosper and LendingClub allow you to borrow from individual investors rather than traditional banks. Not only are the rates better than title loans, but the process is made simple through an online form, helping everyone get the money they need.

Sell assets – Selling valuable items, unique collectibles, or other possessions you no longer use is easier than getting a loan against your car. Many online platforms provide an easy-to-use electronic form to kickstart the selling process.

Smart Strategies if You Do Take an Online Title Loan or Car Title Loan Near Me

Ideally, a title loan must be avoided. Nevertheless, if you find yourself in a tight situation and you’ve exhausted all other superior solutions, follow the following tips to protect yourself:

Shop around – Do not limit your options to a single quote; instead, compare them from various lenders within your state and area. It’s necessary to note that the rates vary widely.

Read the contract – Examine the full amount of the loan, the interest rate, fees, the payment timetable, and penalties. Don’t rush into it – other lenders now even have an online form to make the process easier.

Confirm the value – Investigate your vehicle’s fair market value and resale value in advance so the lender doesn’t underestimate the loan amount you get. A pre-approved online form even gives you guaranteed approval for a certain amount.

Ask about renewals – In other states, title lenders are prohibited from offering to “renew” loans. Treat this option with extreme caution if you are in such a state, as it become very costly.

Pay early – Aim to pay the loan as quickly as possible, potentially even before the 30-day term, which is a smart way to minimize interest fees.

Talk to the lender – If you find it challenging to repay the loan on time, communicate with the lender at your earliest convenience. Verify if they have any hardship options or extensions through an electronic process like an online form. Defaulting is not the solution.

Prioritize the payment – Be prepared to make temporary sacrifices on less expenses to afford your payment when it’s due. Avoiding a default must be a top priority.

Build an emergency fund – Begin setting aside a little each month into savings so you’re not forced back to predatory lenders again for the next surprise expense.

Take credit counseling – To break the borrowing/reborrowing cycle, work with a nonprofit credit counseling agency to consolidate debts and improve your longer-term financial health.

Across the United States, our company is proud to serve customers seeking title loans online with no credit checks. Our commitment to accessibility and convenience has led us to operate in multiple states, ensuring that individuals facing financial challenges can access the financial support they need. Below, you’ll find a comprehensive list of the American states in which our services are available, making it easier than ever for you to explore the options we offer in your area.

| Alabama / AL | Alaska / AK | Arizona / AZ |

| Arkansas / AR | California / CA | Colorado / CO |

| Connecticut / CT | Delaware / DE | District Of Columbia / DC |

| Florida / FL | Georgia / GA | Hawaii / HI |

| Idaho / ID | Illinois / IL | Indiana / IN |

| Iowa / IA | Kansas / KS | Kentucky / KY |

| Louisiana / LA | Maine / ME | Maryland / MD |

| Massachusetts / MA | Michigan / MI | Minnesota / MN |

| Mississippi / MS | Missouri / MO | Montana / MT |

| Nebraska / NE | Nevada / NV | New Hampshire / NH |

| New Jersey / NJ | New Mexico / NM | New York / NY |

| North Carolina / NC | North Dakota / ND | Ohio / OH |

| Oklahoma / OK | Oregon / OR | Pennsylvania / PA |

| Rhode Island / RI | South Carolina / SC | South Dakota / SD |

| Tennessee / TN | Texas / TX | Utah / UT |

| Vermont / VT | Virginia / VA | Washington / WA |

| West Virginia / WV | Wisconsin / WI | Wyoming / WY |

Secured And Unsecured Vehicle Title Loans Explained

Vehicle title loans are great resources for individuals needing quick cash who own a vehicle. They are secured or unsecured, and each type has its merits. A secured loan requires collateral, usually a car, to back up the loan amount borrowed. If you default on payments, your lender can repossess your car. An unsecured loan does not require any collateral, but it carries higher interest rates than a secured loan because no asset backs up the money being lent out.

Considering a loan option is crucial for a borrower’s financial well-being. Borrowers must consider their credit score and financial situation when deciding on a secured or an unsecured vehicle title loan. A secured loan is more suitable for people with good credit who don’t mind paying extra for peace of mind, knowing that nothing will happen to the car. An unsecured vehicle title loan works better for people who need a better credit history but still want access to funds without risking collateral.

Here is a table comparing different aspects of secured and unsecured loans according to LendingTree, highlighting each loan option.

| Secured Loans | Unsecured Loans | |

|---|---|---|

| Interest Rates | Varies by lender and loan type; usually lower than unsecured loans | Varies by lender and credit score; higher than secured loans |

| Example Rates | Auto loan rate: 9.46% APR (2020) Mortgage rate: 3.07% APR (30-year term as of Jan. 24, 2022) | Average APR for credit report with a credit score between 660-679: 24.74% Average APR for credit score 720 or higher: 10.73% (Q1 2021 LendingTree data) |

| Repayment | Fixed, monthly installments over several years; choice between fixed and variable rates | Fixed, monthly payments over a certain number of years; choice between fixed and variable rates |

| Risks | The lender seizes collateral if the borrower defaults; credit report and credit score suffers if payments are missed. | The lender seizes collateral if the borrower defaults; credit report and credit score suffer if payments are missed. |

The table compares secured and unsecured loans based on their interest rates, repayment terms, and associated risks. Secured loans are shown to have lower interest rates than unsecured loans. Secured and unsecured loans are repaid in fixed monthly installments over several years. The major risk associated with secured loans is the potential for the lender to seize the collateral if the borrower defaults. In contrast, unsecured loans do not require collateral but result in collections and court summonses for missed payments. A credit score is a factor in both types of loans, and missed payments negatively impact credit standing. One important consideration for borrowers is carefully assessing their monthly expenses to avoid any difficulties repaying the loan.

Secured loans involve a longer application process due to needing extra information such as proof of ownership and insurance documents. In contrast, unsecured loans require less paperwork with quicker turnaround times since they do not need any form of security from the borrower.

Frequently Asked Questions about Auto Title Loans and Title Loans Near Me

Here are answers to the most common questions consumers have about title lending:

How much money am I able to get with a title loan?

Most lenders loan $25-50% of your car’s resale value, ranging anywhere from a few hundred dollars to several thousand dollars, depending on the value of your vehicle. Older cars qualify for less.

How soon must a title loan be repaid?

Title loans have terms of 30 days or less. Other states set minimum terms of at least 15 or 20 days. The loan agreement specifies your exact due date.

What happens if I can’t repay my title loan on time?

Ask the lender if a single extension is feasible. The lender repossesses your vehicle and sells it to try to recoup their losses if not repaid. Never ignore communication or hide from the lender if struggling to make payments.

Is a title loan like a pawn loan?

There are similarities, but with a pawn loan, the lender physically takes possession of your vehicle. Title loans allow you to keep driving the car while making payments.

Where am I able to get a title loan?

Title lenders operate outside physical storefront locations, but others provide online title loans depending on state laws. Interest rates are capped in states with tighter regulations.

What do I need to qualify for a title loan?

You’ll need your vehicle’s title showing sole ownership, government ID, income source, names of the references, and, in other cases, proof of insurance. Lenders need to verify you own the car.

What types of vehicles are used for title loans?

Cars, trucks, SUVs, motorcycles, RVs, and other automobiles all qualify as collateral. Commercial vehicles like taxis are restricted. And with the advantage of no inspection, the process becomes even more straightforward.

Do title loans hurt my credit?

Taking a title loan has no impact on your credit score since they do not run a credit check. But defaulting on the loan hurt your score. Luckily, with the loans, there’s no proof of income required, making it easier for many individuals to apply.

Is a title loan tax deductible?

Only if you itemize deductions and the loan was used for legitimate business expenses, not personal expenses. Consult a tax professional about deductibility.

The Bottom Line on Car Title Loans and Title Loan Places Near Me

Title loans provide day cash for people with poor credit and few borrowing alternatives. Their convenient store locations and the decision to remove the step of a store visit make applying for a title loan easily accessible. The convenience comes at a very high price, and understanding the risks and exploring other options goes a long way to avoiding desperate borrowing.

Protect yourself by shopping around for the best rates if you resort to a title loan, never borrowing more than needed, reviewing the contract thoroughly, avoiding renewals and reborrowing, and repaying the debt as fast as circumstances allow.

Title loans don’t have to lead to financial disaster with education and discipline. They must still be viewed as an absolute last resort reserved only for cases of true emergency.