Payday loans, known as cash advances or short-term loans, are popular for individuals who need quick access to funds. These loans have high-interest rates and fees, making them controversial in the financial industry.

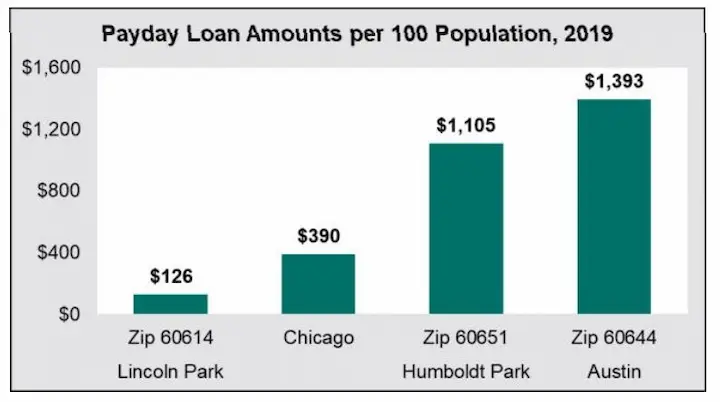

In Chicago, payday lending is regulated by state laws that aim to protect consumers from predatory lenders. Despite the regulations, Chicago Payday Loan Companies and online payday loan options remain prevalent in the city. Various factors, such as unexpected expenses, emergencies, and limited access to traditional banking services, drive the demand for payday loans in Chicago. For many residents in low-income neighborhoods with a bad credit history, payday loan stores, and cash advance loan options have become a common sight on their streets, catering to their short-term financial needs.

Critics argue that payday loans trap borrowers into cycles of debt due to their high costs and aggressive collection practices. The article explores the world of payday loans in Chicago – its benefits and drawbacks, its impact on communities, and what alternatives exist for people seeking short-term financing options.

Understanding Payday Loans

Payday loans are a type of short-term loan borrowed by individuals who need immediate access to cash. There are different payday loans, but they all generally involve borrowing a small amount (usually under $1,000) and repaying it within a few weeks or months. Understanding the eligibility requirements and loan repayment options when taking a payday loan is necessary.

Most lenders require borrowers to have a regular source of income and an active checking account to qualify for a loan. Interest rates on payday loans tend to be high due to their short-term nature, so borrowers must carefully know if they can repay the loan on time without accruing fees or penalties. Payday loans provide quick access to needed funds in emergencies and help individuals with cash advance loan needs; however, they have significant risks and costs to carefully weigh before making any decisions about borrowing money in this way.

What Are the Costs of a Payday Loan?

The costs associated with loan agreements involving payday loans are set by state laws, with fees ranging from $10 to $30 for every $100 borrowed. A two-week payday loan usually costs $15 per $100, according to Experian.

For example, you borrow $100 for a two-week payday loan from a direct lender offering financial services, and they charge you a $15 fee for every $100 borrowed, a simple interest rate of 15%. But since you must repay the loan in two weeks, that 15% finance charge equates to an APR of almost 400% because the loan length is only 14 days. On a two-week loan, that daily interest cost is $1.07.

You multiply that out for a full year—and borrowing $100 costs you $391 if the loan term is one year. Your lender must disclose the APR before you agree to the loan. Payday loans have carried APRs as high as 1,900%. Annual percentage rates (APRs) on credit cards range from 12% to 30%.

With the rise of online loans, people have better access to payday loans without needing to visit a physical location. Here is a table summarizing the costs associated with a payday loan:

| Loan Amount | Fee (15% of Loan Amount) | Loan Term | Daily Interest Cost | Annualized Interest Cost (APR) |

|---|---|---|---|---|

| $100 | $15 | 2 weeks | $1.07 | $391 |

The Pros And Cons Of Payday Loans

Payday loans provide easy accessibility to short-term funds when necessary. The quick, available funds make them desirable for people needing short-term solutions. Payday loans have high-interest rates, which are difficult to pay back. There is a potential for debt if a borrower fails to repay the loan on time.

Pros: Easy Accessibility

The main advantage of payday loans is their easy accessibility. In times of financial emergency, quick approval and short-term lending are necessary to address immediate needs. The absence of credit checks allows people with poor credit scores to access funds they are not otherwise qualified for through traditional lending institutions. The benefit extends to individuals with a limited credit history or no established credit.

Despite the benefits, there are significant drawbacks associated with payday loans. Most notably, the high-interest rates lenders charge mean that borrowers pay significantly more than they borrowed in the first place. Many borrowers find themselves trapped in a cycle of debt as they take new loans to pay off existing ones, further exacerbating their financial situation. As such, while payday loans offer easy accessibility during times of need, potential borrowers must know the cost-benefit analysis warrants taking on this type of loan, given its high-interest rates and long-term consequences.

Quick Funds

Moving on to another subtopic related to the pros and cons of payday loans, we have ‘Quick Funds.’ One advantage of payday loans is their ability to provide quick access to funds. Online options make it even easier for borrowers to apply and receive approval within minutes, allowing them to address immediate financial needs quickly. Eligibility criteria vary depending on the lender, and repayment terms are demanding.

Borrowers must know that interest rates are high and failure to repay the loan on time results in fees or damage to their credit score. Therefore, while quick access to funds is beneficial during times of need, potential borrowers must understand their responsibilities as borrowers and know if taking a payday loan is worth the associated risks and costs.

Regulations Governing Payday Loans In Chicago

Payday loans in Chicago are subject to certain regulations. Interest rates for payday loans are capped at 400%, with a maximum loan amount of $1,000. Repayment terms for payday loans in Chicago are limited to a maximum of 90 days. The total interest and fees for payday loans in Chicago are 22.5% of the total loan amount. Loan limits for payday loans in Chicago are established based on the borrower’s income. Lenders in Chicago must provide a written agreement outlining the loan terms before the loan is issued.

Interest Rates

The interest rates for payday loans in Chicago, Illinois are a necessary aspect of the regulations governing them. Calculating fees and determining APR comparison is necessary to understand the true cost of borrowing money through payday loans. It is necessary to note that borrowers must be eligible to take payday loans, as such financial decisions involve certain criteria to meet before approval.

Once they obtain approval, borrowers must understand the consequences of defaulting on their repayments, which include high late fees and interest charges. Therefore, potential borrowers must carefully weigh their options when taking a payday loan in Chicago and have a solid repayment plan before applying. The loan applications process should be taken seriously, considering the possible impacts of borrowing on their credit rating.

Repayment Terms

Lenders offer flexible options for payment schedules, but borrowers must understand the consequences of defaulting on their repayments, which include high late fees and interest charges. Most lenders allow rollover policies that enable borrowers to extend their repayment deadline by paying only the accrued interest. The policies result in higher costs in the long run, making it essential to make the right Financial Choice.

It is imperative that potential borrowers carefully understand all aspects of repayment before taking a payday loan in Chicago. They must have a solid plan for repayment before applying and avoid borrowing more than they afford to pay back within the given time frame. In doing so, they are able to navigate the complex regulations surrounding payday loans and make informed decisions about if or not this type of lending is right for them.

Loan Limits

Another necessary aspect of Chicago’s regulations governing payday loans is payday loan amounts or loan limits. The City of Chicago regulates the maximum amount lenders are able to offer borrowers, depending on their income and other factors such as credit and payment history. Loan eligibility requirements exist to ensure that only people who can repay the loan are approved. Borrowers typically receive their funds within one business day after approval, making it crucial for them to plan accordingly.

Potential borrowers must understand the restrictions before applying for payday advance loans in Chicago. Borrowers must only take what they need or afford to pay back within the given time frame, resulting in interest charges that further exacerbate their financial difficulties.

How To Apply For A Payday Loan In Chicago

Eligibility criteria for payday loans in Chicago vary by lender but generally require applicants to be at least 18 years old and have a steady income. Most lenders require proof of residency or an active checking account. It is necessary to carefully review the eligibility requirements before starting the loan request to know if you meet all the qualifications.

You need to provide certain documents, such as your government-issued ID, proof of income, and bank statements, when completing the online application form for a payday loan in Chicago. Loan amounts vary from a few hundred dollars to $1,000, depending on the lender and your financial situation.

Repayment terms usually involve paying back the short-term cash advance and interest within two weeks to one month after receiving the loan funds. To apply for a payday loan in Chicago, complete an application online or visit a local storefront location and submit your required documents. The application process is quick and easy, with many borrowers receiving funds within 24 hours of submitting their application.

Avoiding The Pitfalls Of Payday Lending

Payday lending is synonymous with hidden fees and exorbitant interest rates. It is easy to fall into the trap of borrowing more than you can repay, leaving you in a cycle of debt.

But fear not; there are ways to avoid the pitfalls. One way is through financial education. You make informed decisions when it comes to borrowing by learning about personal finance and managing your money effectively, including budget planning and creating a detailed plan for your income and expenses so you know where your money goes each month.

Credit counseling is beneficial, as it guides how to improve your credit score and access lower-interest loans in the future. Debt management programs help people who have fallen into debt by assisting with negotiating payment plans or even consolidating debts into one manageable monthly payment.

Alternatives To Payday Loans In Chicago

As discussed in the previous section, payday loans are risky and expensive for individuals facing financial difficulties. There are alternatives available that help borrowers avoid the pitfalls of payday lending. The alternatives include credit counseling, personal loans, budgeting tips, community resources, and credit unions. Credit counseling services offer free or low-cost advice to individuals struggling with debt. They guide managing finances and creating a realistic budget. Personal loans from banks or online lenders offer more favorable terms than payday loans, including lower interest rates and longer repayment periods.

Budgeting tips such as cutting expenses and increasing income help individuals manage their finances without taking predatory lending practices. Community organizations assist with rent, utilities, food, and other essential needs. Another alternative to know is joining a credit union. Credit unions are nonprofit financial institutions owned by members who share a common bond, such as living in the same community or working for the same employer. They offer lower fees and interest rates on loans compared to traditional banks.

Conclusion

Payday loans in Chicago provide quick cash advance payday loan for unexpected expenses but have a high cost. The irony lies in the fact that small, short-term loan borrowers who need payday loans the most are the ones who end up paying the highest fees and interest rates. Despite regulations governing payday lending in Chicago, borrowers must be cautious when applying for online payday loan lenders to avoid falling into debt traps.

There are alternatives to payday cash advance loans available in Chicago, such as credit unions or community organizations that offer small-dollar loans at lower interest rates. With the help of online cash advances and considering the applicant’s monthly income, these institutions can provide a safer financial option. It is necessary to explore all options before turning to payday lenders to secure financial stability and avoid being trapped in a cycle of debt.

Frequently Asked Questions

Are there online lenders in Chicago that offer payday loans with no credit check?

Some online lenders advertise payday loans with no formal credit check in Chicago. However, most still verify identity and income source to mitigate fraud risks.

What are the potential advantages and disadvantages of payday loans with no credit check in Chicago?

Advantages include quicker access to cash and potentially larger loan amounts. Disadvantages include very high interest rates and repayment difficulty.

How do the interest rates and repayment terms of these loans compare to traditional payday loans?

Rates and terms are similar – APRs over 400% are common. Loan amounts range from $100-$1,000 with 2-4 week repayment required.

What precautions should borrowers take when considering payday loans with no credit check in Chicago to protect their financial well-being?

Avoid lenders who won’t disclose rates and terms upfront. Never pay upfront fees. Make sure you can repay on time to avoid rollovers and fees.

Are there alternative borrowing options for individuals with poor credit in Chicago that are worth exploring?

Alternatives like cash advances, credit union loans, peer lending, credit counseling, employer advances, payment plans, or borrowing from family may be less risky.