Payday loans have become a common way for people to obtain quick cash when they need immediate financial support. Borrowers must understand the limitations and consequences of obtaining multiple payday loans simultaneously. The question arises, how many payday loans must you have at once?

There is no set limit on how many payday loans one must obtain simultaneously, but having multiple payday loans leads to significant debt and financial instability. Many individuals who rely on such loans are trapped in a cycle of borrowing and repayment, leading to more stress and anxiety. PaydayDaze discusses the risks and potential consequences of obtaining multiple payday loans and explores alternatives available to people seeking financial assistance.

Overview Of Payday Loans

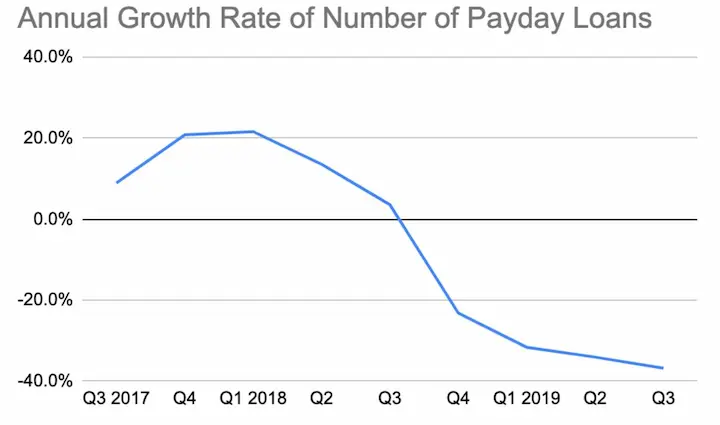

Payday loans provide quick cash to individuals needing emergency funds but have high-interest rates and fees. Individuals must carefully review if obtaining multiple payday loans at once is financially feasible or sustainable in the long run despite the resources available for managing payday loans responsibly. Approximately 12 million Americans are estimated to take out a payday loan each year, according to Bankrate.

| Statistics | Data |

|---|---|

| Cost of payday loans in states with fewer protections | 4 times higher than in other states |

| Average payday loan term | Roughly two weeks |

| Default rate on payday loans | 1 in 5 borrowers |

| Default rate on online installment loans | More than half of all borrowers |

| Percentage of borrowers who reborrow payday loans | 80% within 30 days |

| Estimated number of Americans taking payday loans/year | 12 million (per most recent CFPB data) |

Many countries have implemented regulations requiring affordability assessments before approving loan applications to protect consumers from predatory lending practices. Debt consolidation companies and credit counseling agencies offer services aimed at helping borrowers manage their debts through repayment plans and budgeting tools. Below is a step-by-step process for obtaining any payday loan.

- Research online payday lenders.

- Check eligibility requirements.

- Fill out an application.

- Submit your application

- Wait for approval

- Receive funds

- Repay the loan

Regulations And Limitations

State laws regarding payday loans vary from state to state, with various states having more stringent regulations than others. Financial institutions have policies and restrictions in place, such as loan caps, interest rate limits, and repayment terms. Loan caps are one of the most common restrictions on payday loans, which limit the number of loans a person must have at any given time.

State Laws

State laws play a key role in determining the regulations and limitations of borrowing regarding payday loans. Government oversight is necessary to verify that lenders operate within legal boundaries and do not exploit borrowers with high-interest rates or hidden fees. Each state has its own set of rules governing payday lending, with various states imposing strict limits on the number of loans an individual must have at once, while others impose no restrictions whatsoever.

Financial literacy plays a key role in navigating the world of payday lending, as individuals must know their rights and responsibilities when obtaining such short-term loans. Understanding state laws and financial literacy helps protect borrowers from falling into debt traps caused by multiple payday loans.

Financial Institutions

Financial institutions play a significant role in regulating payday loans. Credit unions provide an alternative to high-interest payday loans by offering low-cost, short-term loans with flexible repayment terms. Debt consolidation services offered through financial institutions help individuals manage their outstanding debts and avoid the cycle of obtaining multiple payday loans.

Utilizing such resources enables borrowers to gain better control over their finances and reduce their reliance on risky lending practices. Individuals must explore all available options before taking payday loans as a last resort.

Loan Caps

Loan caps refer to laws or regulations that limit the amount of money a borrower receives from a lender and the interest rates and fees charged on such loans. Loan caps protect consumers from predatory lending practices by preventing lenders from charging exorbitant fees and high-interest rates on short-term loans. Implementing a loan cap makes borrowers less likely to fall into debt traps caused by unaffordable repayment terms.

Debt consolidation and credit counseling services offered through financial institutions assist individuals in managing their debts while avoiding the need for payday loans altogether. Such options provide borrowers with more affordable ways to manage their finances without falling into debt cycles caused by multiple payday loans.

State-Specific Restrictions

Different states in the US have varying payday loan caps and regulations. Various states impose strict limitations on the number of loans an individual must obtain simultaneously, while others allow multiple cycles with certain restrictions.

A borrower in California must stay within one outstanding loan from any lender or obtain another until you repay the previous one. Texas imposes no such limits but requires lenders to offer repayment plans for people struggling to meet their obligations.

Borrowers must review debt consolidation options that help them manage their finances more efficiently. You must research and understand relevant policies before obtaining payday loans, as they have high-interest rates and hefty fees.

Understanding Interest Rates And Fees

Understanding interest rates and fees is key when exploring payday loans, as they quickly accumulate and lead to a cycle of debt. Interest rates on such loans are higher than traditional bank loans or credit cards, usually reaching triple digits. Fees such as origination fees, late payment fees, and prepayment penalties add up quickly.

Borrowers must compare loan terms from various lenders to get the best rate. Alternative borrowing options, such as personal loans or debt consolidation, are worth exploring if you have multiple payday loans with high-interest rates. Such options potentially lower your overall monthly payments and improve your credit rating in the long term.

Risks Of Taking Out Too Many Loans

There are various risks associated with obtaining too many payday loans.

- High-interest rates are a major concern when obtaining too many loans, as borrowing costs increase with each loan.

- Accumulating debt is a major risk when obtaining too many loans, as the total amount owed quickly becomes unmanageable.

High-Interest Rates

Lack of financial literacy and understanding of how interest works are detrimental when managing one’s finances. You must understand that obtaining too many payday loans leads to high-interest rates, which results in a cycle of debt sustainability.

Many individuals who obtain multiple loans fail to comprehend the consequences of such high-interest rates, leading them deeper into financial trouble. Borrowers must educate themselves on such factors before obtaining any loan, especially payday loans, with their notorious reputation for exorbitant interest rates.

Accumulating Debt

Borrowers accumulate more debt than they handle due to the high-interest rates and fees associated with payday loans. Accumulating too much debt becomes overwhelming for individuals struggling to make ends meet. Seeking help from professionals through services like debt consolidation or credit counseling is beneficial in managing one’s finances and avoiding further financial distress.

Responsible Use Of Payday Loans

Payday loans provide a quick financial solution for unexpected expenses, but you must use them responsibly. Responsible budgeting and planning help to avoid the need for a payday loan in the first place. Exploring other options, such as debt consolidation or alternative borrowing options, is more financially beneficial in the long run if borrowing becomes necessary.

Credit counseling services are available to assist with managing debt and improving overall financial literacy. You must fully understand the terms and conditions of any payday loan before accepting it and only repay what you are able to repay on time realistically.

Conclusion

Payday loans offer a quick financial solution for people needing emergency funds. You must understand the regulations and limitations surrounding such loans before taking them out. Each state has its restrictions on the number of loans one must have at once and the interest rates and fees they must review. Multiple loans seem attractive, but you must weigh the risks of obtaining too many loans. Borrowers must review the potential damage to credit scores and long-term financial stability.

Responsible use of payday loans means borrowing what you need and being able to pay back the loan in full within the agreed-upon timeframe. Individuals must explore alternative options for borrowing money before resorting to payday loans. Budgeting, seeking assistance from family or friends, or even negotiating payment plans with creditors are all avenues to review.

Frequently Asked Questions

What is the maximum number of payday loans I can have at one time?

Regulations on the maximum number of payday loans allowed at once vary by state. Some prohibit more than one loan, while others cap at 2-4 loans per borrower across all lenders.

Is there a legal limit to the number of payday loans a person can have simultaneously?

Yes, most states impose legal limits ranging from 1-4 loans at a time per borrower. Rules vary on amounts, loan terms, and renewals based on the specific state’s regulations.

Do the rules regarding the maximum number of payday loans allowed vary by state or region?

Yes, regulations on maximum simultaneous payday loans differ significantly by state. Some ban payday lending while others restrict to 1-4 loans per borrower across lenders.

Can someone take out multiple payday loans from different lenders at the same time?

In states without a central database, it may be possible but extremely risky financially. Most states prohibit more than one payday loan at once to prevent excessive debt.

What happens if I get too many payday loans and can’t repay them all? Will I go to jail or face legal problems?

Defaulting on multiple payday loans won’t land you in jail but can lead to aggressive collection calls, lawsuits, wage garnishment, and long-term damage to your credit score.