Defaulting on a payday loan and closing the associated bank account have serious consequences. Payday loan lenders try to collect the debt through other means, and borrowers face legal action, including wage garnishment or asset seizure. Defaulting on a payday loan harms the borrower’s credit score, making it challenging to access credit in the future.

Communication with payday lenders is vital, as they provide payment plans or alternative options to help repay the debt. Ignoring the debt and closing the account is not a solution, and borrowers must be responsible for not having serious consequences.

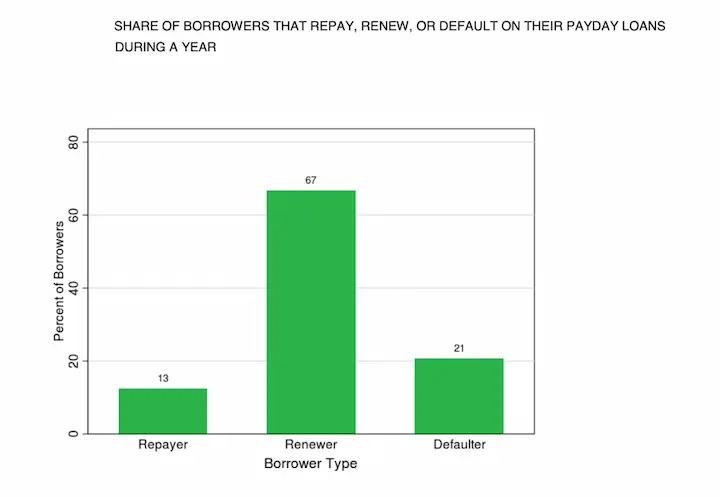

Understanding Payday Loans And Default

Online payday loans are short-term loans with high-interest rates and fees. They are to help people get through a financial emergency or unexpected expense until their next payday. The borrower usually writes a post-dated check for the full loan amount and fees, which the lender cashes on the borrower’s next payday.

Defaulting on a payday loan means the borrower must make their scheduled payments on time. It results in various consequences, including other fees, higher interest rates, and damage to the borrower’s credit score. The lender takes legal action against them if the borrower continues to miss payments, which results in wage garnishment or even seizure of assets.

What Are The Alternatives To Defaulting Payday Loans?

Alternatives to defaulting on payday loans emphasize exploring all options before defaulting to prevent negative consequences. Listed below are the alternatives to Payday Loans and their uses.

Negotiate an extended payment plan.

Negotiating an extended payment plan is a common strategy for managing debt and avoiding default. Contact the creditor or lender and ask for a longer period to repay the debt with smaller payments over time. By securing a loan on time, you can avoid the stress and complications of defaulting.

Seek assistance from financial counseling services.

Financial counseling services can help borrowers assess their financial situation, create a debt management plan, and provide guidance on better managing their money. It can prevent defaulting on their payday loans and safeguard their credit rating. Borrowers should also carefully review their loan agreement before borrowing to ensure they understand its terms and conditions, which can prevent misunderstandings and defaulting on the loan.

Seeking assistance from financial counseling services is an effective way to manage debt and achieve financial stability. Financial counseling services offer a range of benefits to individuals struggling with debt, including personalized guidance on budgeting, debt management, and long-term financial planning. Individuals learn effective strategies for negotiating repayment plans with creditors by working with a qualified credit counselor.

Obtaining a personal loan from a bank or credit union.

Obtaining a personal loan from a bank or credit union is a viable option for individuals who need to borrow money and avoid the high-interest rates and fees associated with payday loans. A debt consolidation loan from a loan provider such as a bank or credit union is a good alternative to payday loans, as they offer lower interest rates, flexible repayment options, and fewer fees.

Use credit cards with lower interest rates.

Credit cards with lower interest rates can help individuals manage their debt more effectively. By transferring balances and consolidating debt, individuals can reduce their overall interest payments and free up financial resources to better manage their finances. Transferring debt to a credit card with a lower interest rate and working with a credit counselor to implement a comprehensive debt management plan can greatly improve financial stability.

Using credit cards with lower interest rates is a strategy for managing credit card debt and minimizing financial damage. Credit cards with lower interest rates help reduce borrowing costs and make payments more manageable. They are helpful for individuals who are struggling to pay off high-interest debt, like payday loans, and decrease overall loan costs. Considering the type of loan can impact the choice of tools for managing debt.

Sell unwanted items.

Selling unwanted items is a great way to generate extra income and declutter one’s home. Selling unwanted items generates extra income and pays off credit card debt while creating a more organized and clutter-free living space.

What Are The Legal Implications Of Defaulting

Defaulting on a loan or other financial obligation have serious legal implications, depending on the default’s specific circumstances, the type of loan, and the contract terms involved. Here are a few examples.

- Collection efforts – The lender engages in various collection efforts to recover the money owed if one defaults on a loan. It includes sending collection letters or making phone calls, hiring a collection agency, or even suing one in court. A collection agency can take various measures to recover the debt on behalf of the lender.

- Credit damage – Defaulting on a loan hurts credit score, which makes it harder to obtain credit in the future. A default remains on a credit history report for up to seven years, impacting one’s ability to secure new loans or lines of credit.

- Asset seizure – Lenders have the legal power to repossess the borrower’s home or automobile if the borrower defaults on a secured debt like a mortgage or car loan.

- Legal action – Lenders resort to legal action if they cannot recover past-due loan payments via other channels, such as working with a collection agency. It includes filing a lawsuit against you, having your salary or bank accounts garnished by court order, or even putting a lien on your property.

The Risks Of Closing A Bank Account

Closing a bank account requires properly addressing outstanding debts to prevent financial consequences in late fees, overdraft fees, and potential legal action. Defaulting on a payday loan causes damage to one’s credit score and results in collection actions taken by a lender, like a wage garnishment or legal action.

- Fees – Other banks charge a fee for closing an account, especially if one closes it within a certain period after opening the account. Be aware of potential bank fees and avoid incurring additional costs by closing an account outside of any specified time frame.

- Credit score – Closing a bank account affects credit score if linked to other financial products, like loans or credit cards. The average age of their credit accounts affects their credit score. Consider the impact of bank fees on credit ratings before closing an account.

- Overdrafts – The bank force individuals to pay overdrafts or other penalties before terminating their account. It can sometimes include bank fees associated with account closure, so clear any outstanding balances or penalties before closing the account.

- Direct deposits and automatic payments – Borrowers need to update their information with the companies or individuals to prevent missing payments or transactions if they have any automatic payments or direct deposits in their bank account. Ensure that any bank fees are accounted for when updating payment information.

- Loss of banking history – Closing a bank account results in losing their banking history with that institution. It impacts the ability to obtain future credit or other financial products. Weigh the potential benefit of avoiding bank fees against the loss of banking history before deciding to close an account.

What Are The Strategies For Minimizing Damage?

The strategies for minimizing damage caused by debt include negotiating with creditors, creating a budget, seeking assistance from credit counseling agencies, consolidating debts, and exploring debt settlement. Borrowers must prioritize debt repayment and seek help when needed. Its strategies help individuals manage their finances responsibly and work towards becoming financially stable again.

- Negotiating with creditors. Contacting creditors and explaining their situation leads to more flexible repayment plans or reduced interest rates. It helps make monthly payments more manageable and minimizes damage to credit scores. It’s also essential to be aware of the impact of credit checks during negotiations or when applying for new credit products, as these can also affect credit scores.

- Creating a budget. Creating a budget help individuals track their expenses and prioritize necessary payments. A crucial aspect of managing personal credit is understanding the credit utilization ratio, representing the proportion of available credit used. To allocate more money toward debt repayment, you must identify areas where you can cut expenses.

- Seeking assistance from credit counseling agencies. Credit counseling agencies help individuals create a feasible repayment plan and provide financial education to avoid future financial difficulties. They can also help understand and interpret credit bureau reports, enabling individuals to make informed decisions about their credit management.

- Consolidating debts. Consolidating debts makes monthly payments more manageable by combining several debts into one payment with a lower interest rate. Debt consolidation may also positively impact the credit utilization ratio and overall credit health.

- Exploring debt settlement. Debt settlement involves negotiating with creditors to pay less than the total amount owed. Credit ratings take a hit, but paying off debts can help people save money. Be aware that credit bureaus report settled debts, and this information can negatively influence future borrowing opportunities.

Payday Loans Regulations

State laws limit payday loans, cash advances, and advance loans between $100–$1,000. Loan terms average two weeks. Loans have 400% APR or greater. Borrowing $100 costs $15–$30 in finance charges. Its financing costs result in 390–780% APR for two-week loans. Shorter-term loans have higher APRs. States without caps charge more for cash advances.

| Scenario | Loan Amount | Loan Term | APR | Finance Charge |

| A | $100 | 2 weeks | 400% | $15 |

| B | $250 | 1 week | 450% | $30 |

| C | $500 | 3 weeks | 500% | $50 |

| D | $750 | 2 weeks | 550% | $75 |

| E | $1000 | 4 weeks | 600% | $100 |

Explanation of each scenario, according to CFA:

To apply for a payday loan, customers must complete an online form and provide a debit card as the payment method. Once the application is approved, the lender will transfer the funds to the applicant’s bank account. However, knowing the credit limit customers can request is crucial, as the amount may vary between providers.

- Scenario A – It represents a payday loan, with a loan amount of $100 and a two-week loan term. The APR is 400%, the average for payday loans, and the finance charge is $15, which is at the lower end of the range. This scenario doesn’t involve a conventional loan and has a higher cost of credit.

- Scenario B – It represents a larger loan amount of $250 but a shorter loan term of one week. The APR is slightly higher at 450%, and the finance charge is $30 at the higher end of the range. Still, it’s not a conventional loan option and has a considerable cost of credit.

- Scenario C – It represents a loan amount of $500 with a three-week loan term. The APR is higher at 500%, and the finance charge is $50, which is in the middle of the range. However, it lacks the advantages of a conventional loan and comes with an expensive cost of credit.

- Scenario D – It represents a larger loan amount of $750 with a two-week loan term. The APR is even higher at 550%, and the finance charge is $75, at the higher end of the range. Despite the higher loan amount, it’s not a conventional loan and carries a significant cost of credit.

- Scenario E – It represents the maximum loan amount of $1000 with a four-week loan term. The APR is the highest at 600%, and the finance charge is $100, at the higher end of the range. This scenario also misses the benefits of a conventional loan and has an elevated cost of credit.

Bottom Line

Closing the bank account is not an option if one defaults on a payday loan and faces serious legal and financial implications. It makes it much more difficult for lenders to recoup their losses. Lessen the blow by working out a payment extension with the lender or getting help from a credit counseling program. One solution worth looking into is personal loans with lower interest rates and more forgiving payback terms.

Frequently Asked Questions

What are the consequences if I close my bank account and default on a payday loan?

Closing your account won’t erase the debt, which can be sent to collections and sued upon. Your credit score will plummet and wages may be garnished. Fees and interest still accrue.

Can the payday lender still pursue collection actions if I close my bank account to avoid repayment?

Yes, closing the bank account does not cancel the legal obligation to repay the loan. Lenders can employ collection agencies, lawsuits, and other means to recover the debt.

Will closing my bank account protect me from legal actions or fees associated with a defaulted payday loan?

No, closing the account provides no protection from collections or legal consequences. You still owe the full amount plus additional late fees and interest charges.

What impact will defaulting on a payday loan and closing my bank account have on my credit score and financial future?

This will devastate your credit score, making it much harder to qualify for credit or loans in the future. Legal judgments will also harm your finances.

Are there alternative strategies for dealing with payday loan debt that do not involve closing my bank account?

Instead negotiate an extended payment plan, consolidate/refinance the loan, borrow from family or friends, obtain debt counseling, or consider bankruptcy only as a last resort.