The statute of limitations on payday loans in Rhode Island is ten years, meaning that payday loan companies have up to ten years to file a lawsuit against a borrower who has defaulted on a payday loan. It is worth noting that the statute of limitations on debt in Rhode Island differs depending on the type of debt and the case’s specific circumstances.

It is advisable to seek the guidance of a lawyer if there are any concerns regarding the statute of limitations on a specific debt. Individuals struggling with payday loan debt find assistance through resources like credit counseling and debt consolidation programs, which help them manage and repay their debt.

Understanding The Basics Of Statute Of Limitations

Payday loans are short-term loans that individuals get quickly and easily, with little or no credit check required. Rhode Island payday loans are legal, but certain restrictions and regulations are in place to protect borrowers from predatory lending practices. Rhode Island law sets a limit of $500 on payday loans offered in the state. The minimum loan term is 13 days, and there is no maximum loan term.

Borrowers must provide the lender with a post-dated check for the loan amount with fees or provide authorization for the lender to withdraw the funds directly from their bank account on the due date to obtain a payday loan in Rhode Island.

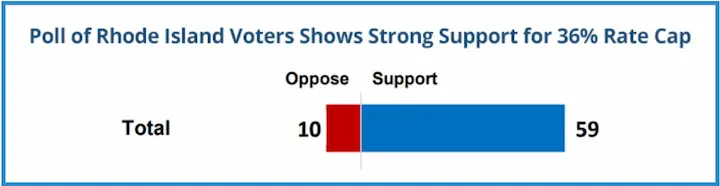

Payday Loans in Rhode Island Regulations

Rhode Island allows payday loans. The maximum amount of payday loans that borrowers get in Rhode Island is $500. There is no maximum loan period; the minimum loan term is 13 days.

APR goes up to 261%. There are two rollovers. Crimes committed against debtors are forbidden.

| Loan Terms | Scenario 1 | Scenario 2 | Scenario 3 |

| Loan Limit | $500 | $300 | $700 |

| Minimum Loan Term | 13 days | 13 days | 13 days |

| Maximum Loan Term | None | None | None |

| APR | 261% | 200% | 300% |

| Finance Charge | 10% of the amount advanced | 7% of the amount advanced | 12% of the amount advanced |

| Rollovers Allowed | 2 | 1 | 3 |

| Criminal Actions Prohibited | Yes | Yes | Yes |

Explanation of scenario, according to UStatesLoans.

Scenario 1. Lenders set the loan limit at $500, the maximum amount borrowers borrow in Rhode Island. The minimum loan term is 13 days, with no maximum loan term. The lender charges an APR of up to 261%, and they cap the finance charges at 10% of the amount advanced. They allow borrowers to have two rollovers and prohibit them from committing criminal actions.

Scenario 2. Lenders set the loan limit at $300, less than the maximum loan amount allowed in Rhode Island. They set APR at 200%, lower than the maximum APR allowed. The minimum loan term remains at 13 days, with no maximum loan term. Finance charges are capped at 7% of the amount advanced, which is lower than the maximum finance charge allowed. Only one rollover is allowed, and criminal actions against borrowers are prohibited.

Scenario 3. Lenders set the loan limit at $700, higher than the maximum loan amount allowed in Rhode Island. They set APR at 300%, higher than the maximum APR allowed. The minimum loan term remains at 13 days, with no maximum loan term. Finance charges are capped at 12% of the amount advanced, which is higher than the maximum finance charge allowed. Three rollovers are allowed, and criminal actions against borrowers are prohibited.

What Are Other Options For Payday Loans in Rhode Island?

Other Rhode Island Payday Loans options include government assistance programs, credit unions, credit counseling, credit card cash advances, borrowing from family or friends, and peer-to-peer lending platforms. Government assistance programs like SNAP, TANF, LIHEAP, and Medicaid support eligible residents experiencing financial difficulties.

Credit unions give their members lower interest rates on loans and credit cards and focus on offering financial services. Credit counseling provides education and resources to help clients improve their financial stability, negotiate with creditors and develop a debt management plan.

Credit card cash advances, borrowing from family or friends, and peer-to-peer lending platforms are other alternatives to payday loans that offer various advantages like flexibility, accessibility, and competitive interest rates.

Government Assistance

A government assistance program refers to a program or policy that a government creates to provide financial or other types of aid to individuals or groups in need. Its programs include unemployment benefits, food assistance, housing subsidies, and healthcare assistance.

The programs aim to help improve the living standard for economically or socially struggling individuals. Their funds are from taxes, government debt, or other means. Government assistance programs vary widely in scope, eligibility requirements, and the types of aid they provide.

Credit Unions

Credit unions are member-owned and non-profit financial institutions that offer various financial services, like savings accounts, checking accounts, loans, and credit cards. They are smaller than traditional banks and focus on serving specific communities or groups of people.

The main advantage of credit unions is that they offer lower interest rates on loans and credit cards because their primary goal is to provide financial services to their members rather than generate profits for shareholders. Credit unions are cooperative financial institutions that provide members with various services, including access to loans that borrowers repay in installments over a while.

Credit Counseling

Credit counseling is a non-profit service organizations offer to help individuals better manage their finances and improve their credit. A credit counselor works with clients to develop a budget, create a debt management plan, and provide education and resources to help clients achieve financial stability.

A counselor reviews a client’s income, expenses, debts, and credit report to identify areas where the client has to make changes to improve their financial situation during a credit counseling session. The counselor negotiates with creditors on behalf of the client to reduce interest rates or waive fees.

Credit Card Cash Advance

A credit card cash advance is a short-term loan that borrowers obtain at an ATM or bank using their credit card. The amount that applicants borrow depends on the credit limit of the card and the available cash advance limit. Cash advances are subject to high fees and interest rates, and the interest starts accruing immediately.

There are several advantages to credit card cash advances. The advantage is that they are easily accessible, as borrowers use their credit cards to obtain the necessary cash. Another advantage is that they are useful for various purposes, like covering unexpected expenses or emergencies.

Family or Friends

Borrowing money from family or friends is a useful alternative to payday loans. They offer lower or no interest rates, saving the borrower money. The advantage of borrowing from family or friends is offering more flexible repayment terms, as the lender works with the borrower to set up a repayment schedule that works for both parties. Another advantage is that borrowing from family or friends is a convenient and accessible option.

Peer-to-peer Lending Platforms

Peer-to-peer lending platforms provide an alternative option for online borrowers seeking installment loans, connecting them with individual investors lending money. Its platforms offer competitive interest rates and flexible repayment terms.

Borrowers must provide information about their income, employment, and credit history to apply for a loan on a peer-to-peer lending platform. The platform uses its information to assess their creditworthiness and assigns them a credit rating.

What are the responsibilities of borrowers after the statute of limitations expires?

The statute of limitations is the legal time limit within which a creditor sues a borrower to recover a debt. The creditor no longer sues the borrower to collect the debt once the statute of limitations has expired. The borrower still has responsibilities even after the statute of limitations has expired, depending on the jurisdiction and circumstances. Here are the common responsibilities that borrowers have.

- Acknowledge the debt – A verbal or written acknowledgment includes the amount owing and the payback arrangements. Acknowledging a debt means one commits to repaying it, which has legal consequences.

- Make voluntary payments – The borrower still be under a moral or ethical responsibility to pay the loan even if the creditor is unable to bring legal action against them. Making voluntary payments help improve the borrower’s credit score.

- Respond to requests for information – The borrower must still respond to requests about the debt, like providing proof of payment or disputing the debt if it is inaccurate or invalid.

- Report forgiven debt as income – Borrowers must report the forgiven amount as income for tax purposes if the creditor forgives the debt.

How To Protect the Financial Future?

Protecting the financial future involves securing their financial situation and preparing for unforeseen events that affect finances. Here are key steps individuals take to protect their financial future.

- Create a budget. A budget helps individuals manage their money effectively by tracking their income and expenses. It helps one identify areas where they cut back on expenses and save more money.

- Build an emergency fund. An emergency fund provides a financial safety net in case of unexpected expenses or loss of income. Experts recommend saving at least three to six months of living expenses in an emergency fund.

- Protect assets with insurance. Insurance provides financial protection in case of accidents, illness, disability, or other unforeseen events. Examples include health insurance, life insurance, disability insurance, and homeowner’s or renter’s insurance.

- Invest for the long-term. Investing helps individuals grow their wealth over time, but individuals must choose investments that align with their risk tolerance and investment goals. Work with a financial advisor to create a diversified investment portfolio that suits individual needs.

- Retirement plan. Retirement planning involves setting goals, estimating expenses, and creating a savings plan to know they have enough money to support their lifestyle in retirement.

- Monitor credit score. Credit scores impact the ability to obtain credit or loans and affect the interest rates consumers receive. Regularly monitoring the credit score and credit report helps individuals identify and correct errors and improve their overall creditworthiness.

Borrowers are able to help protect their financial future and achieve long-term financial goals by taking steps and being proactive in managing their finances.

Bottom Line

The statute of limitations on payday loans in Rhode Island is an aspect that lenders and borrowers need to understand. A legal timeframe determines when creditors must repay debts or face legal action for non-payment. Borrowers are still responsible for their debts even after the statute of limitations expires. They still face legal action and debt collection efforts if they default on their loans.

Borrowers must protect their financial future by being mindful of their borrowing practices and making timely payments to prevent negative consequences. PaydayDaze makes fair lending practices while maintaining financial stability for all parties involved by understanding and adhering to its regulations.

Frequently Asked Questions

What is the statute of limitations for payday loans in Rhode Island, and how does it apply to these types of loans?

The statute of limitations for payday loans in Rhode Island is three years. This means lenders can’t sue borrowers for repaying payday loans after three years have passed since the borrower defaulted. The debt still exists but becomes legally unenforceable.

Can payday loan lenders take legal action against borrowers in Rhode Island after the statute of limitations has expired?

No, payday lenders in Rhode Island cannot take legal action or sue borrowers to collect on payday loan debt after the 3-year statute of limitations has expired. The debt still exists but is no longer legally enforceable through the courts.

How long is the statute of limitations for collecting on payday loan debts in Rhode Island?

The statute of limitations for collecting on payday loan debt in Rhode Island is three years. After three years have passed from the borrower’s default or last payment, the lender loses the ability to sue or take legal action.

Are there any exceptions or circumstances that could extend the statute of limitations for payday loans in the state?

The statute of limitations may be extended if the borrower makes a partial payment, enters a repayment plan, acknowledges the debt in writing, files bankruptcy, or leaves the state for a period. These can restart the clock, giving lenders more time to collect.

What steps can borrowers take to ensure they understand and adhere to the statute of limitations on payday loans in Rhode Island to protect their rights?

Borrowers should confirm the statute is three years, mark default dates, avoid making payments/acknowledgments after the time limit, seek legal help if sued over an expired debt, and learn how to use the statute as a defense against collection.